Executive Summary

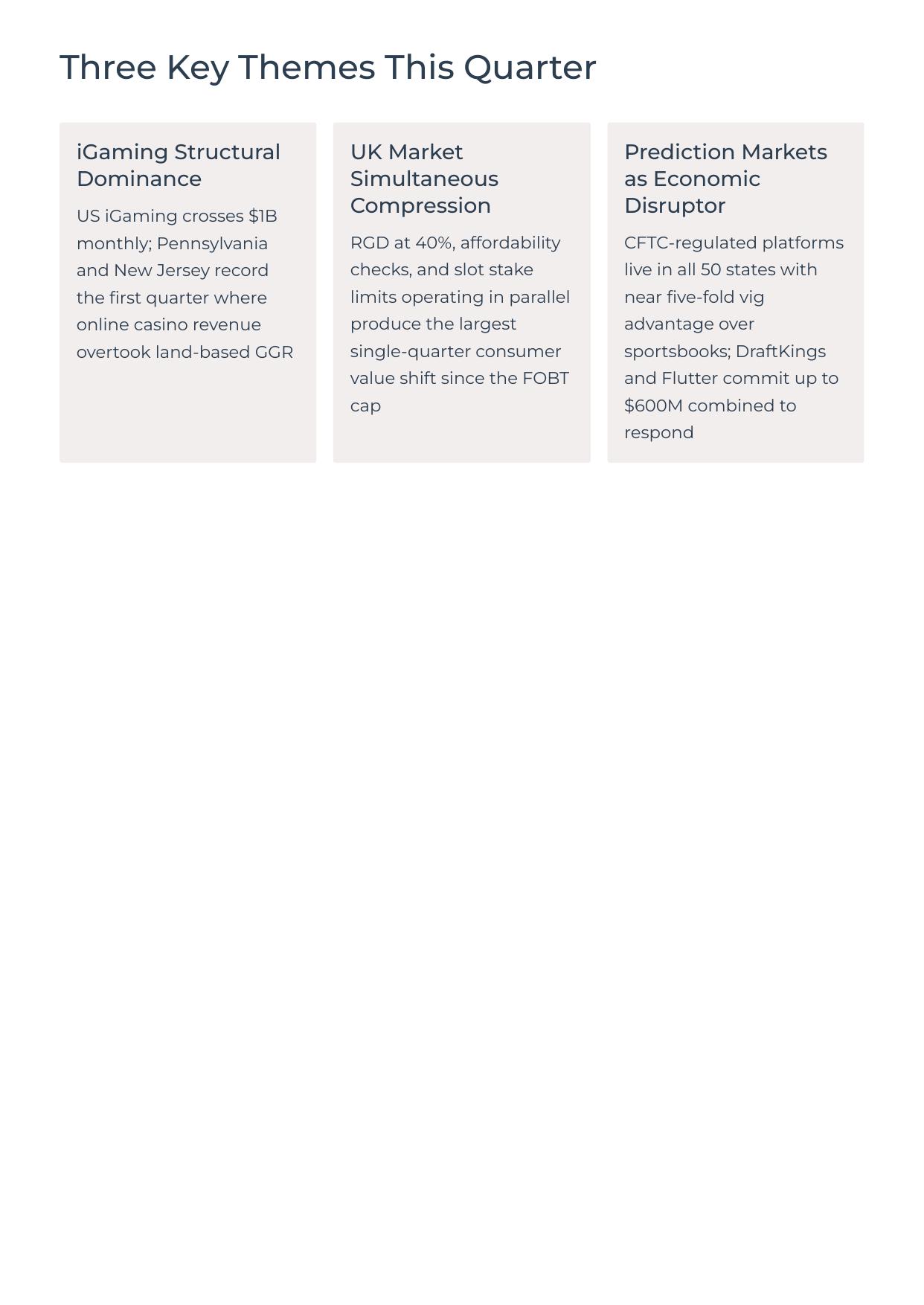

Q2 2026 arrived at the intersection of three developments that were each, individually, the kind of thing a boardroom spends a year preparing for. The UK market absorbed two structural interventions simultaneously: Remote Gaming Duty rising to 40% from 1 April and the UKGC affordability check phase one from February, both operating alongside the ongoing slot stake limit framework. US iGaming crossed its first billion-dollar monthly revenue threshold in April and delivered 20.7% quarterly growth while traditional casino gaming expanded at 2.1%. And prediction markets, operating under CFTC commodity exchange rules in all 50 US states, emerged with near five-fold pricing advantages over conventional sportsbooks, forcing the two largest US digital operators to commit up to $600 million combined to build exchange infrastructure for a channel whose regulatory framework is still being written.

The channel migration story is no longer forecast. In Pennsylvania and New Jersey, online casino revenue overtook land-based for the first time in 2025, and Q2 2026 is reinforcing that outcome. Regional US land-based operators saw foot traffic fall 8.3% year-on-year in April. European online gambling channels are growing at 6.9% annually against a broadly flat land-based estate. These divergences are structural, not temporary.

The UK data warrants particular attention this quarter because compression is happening simultaneously from multiple directions. A May 2026 consumer survey found 58.6% of UK players reporting that bonuses, odds, and offers had worsened over the previous twelve months, with just 1.5% saying conditions had improved.

Three Key Themes This Quarter